My Way? Not at the Fed

Source: Air Mail, “Assignment: Sinatra"

Frank Sinatra earned the nickname "Chairman of the Board" by doing things entirely on his own terms. Commanding the room, setting the tone, and making sure everyone knew the show ran his way. On May 13, the Senate confirmed Kevin Warsh as the 17th chair of the Federal Reserve. Although Warsh may be the chairman, he cannot do things exactly his way, as we’ll talk about below. Warsh arrives with an agenda, a reputation, and a clear sense of how he wants to run the room. Whether he can and how quickly will depend entirely on his ability to bring the rest of the committee along with him.

How the Federal Reserve Works

Source: Federal Reserve, DoubleLine

The Federal Reserve is the central bank of the United States. Congress has mandated that it conduct monetary policy "so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates".1 This directive is commonly known as the dual mandate, since stable prices and maximum employment are generally understood to create the conditions in which interest rates settle at moderate levels on their own. Executing on that mission involves a web of institutions, committees, and tools that directly affect many aspects of financial lives, from the interest rate on an auto loan to the yield on a 10-year Treasury bond.

Source: The Federal Reserve

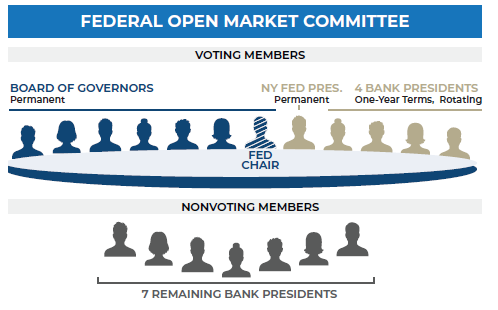

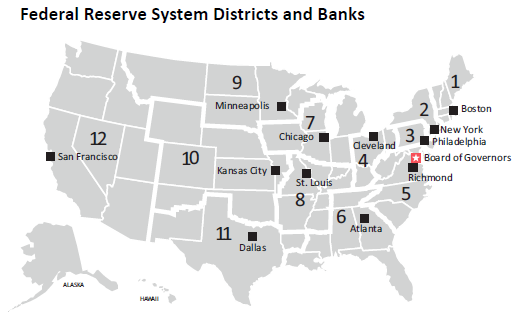

As seen in the images above, The Fed operates through two distinct bodies. The Board of Governors, based in Washington D.C., consists of seven members appointed by the President and confirmed by the Senate, including the Fed Chair, who leads the board and serves as the face of the institution. Alongside them sits the Federal Reserve System's 12 regional Reserve Banks, each headed by a bank president who represents the economic conditions of their district.

These two bodies come together in the Federal Open Market Committee, the FOMC, the 12-person panel that actually sets interest rate policy. Of those 12 votes, seven belong permanently to the Board of Governors. The President of the New York Federal Reserve holds a permanent seat as well, reflecting New York's role as the center of U.S. financial markets. The remaining four votes rotate annually among the other 11 regional bank presidents, meaning seven bank presidents are present at every meeting but sit as nonvoting members in any given year.

The Fed Toolkit

The Fed has several tools at its disposal, but we will look at the two most popular below. Understanding both tools matters because the incoming chair has strong opinions about how each should be used.

Source: Federal Reserve H.4.1 Statistical Release | FRED, Federal Reserve Bank of St. Louis

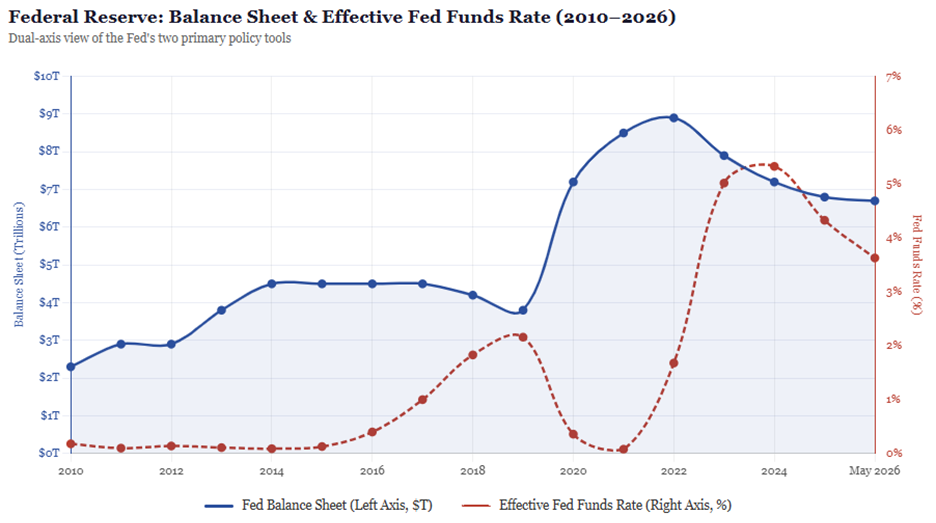

The first tool is the federal funds rate; the interest rate banks charge each other for overnight lending. Think of it as the economy's water pressure. The Fed controls the main valve, and every pipe downstream: mortgage rates, auto loans, credit cards, corporate borrowing feels the change. Turn it up and credit tightens across the board; turn it down and money flows more freely through the system. The rate itself never appears on your monthly statement, but it quietly determines the terms of nearly every financial transaction in the country.

The second tool is open market operations using the Fed’s balance sheet, a less intuitive but equally powerful lever. Since the 2008 financial crisis, the Fed has accumulated over $6 trillion in Treasury bonds and mortgage-backed securities through a process known as quantitative easing, or QE. When the Fed buys these assets, it injects liquidity via money into the financial system and pushes long-term interest rates lower, even when the federal funds rate has already been cut as far as it can go. The reverse, quantitative tightening (QT), involves allowing those securities to mature without replacement, gradually shrinking the balance sheet and putting upward pressure on longer-term borrowing costs. Think of the interest rate tool as the short-term dial and open market operations as the long-term dial.

Who is Kevin Warsh?

Source: Google Gemini

Kevin Warsh is not a career central banker, nor an academic economist in the mold of Ben Bernanke or Janet Yellen. He is a Stanford and Harvard Law-trained finance and policy lawyer who came to the Fed by way of Morgan Stanley's M&A practice and the Bush White House, where he helped navigate the federal response to major corporate accounting scandals and the passage of Sarbanes-Oxley. Appointed to the Board of Governors in 2006 at age 35, the youngest governor ever confirmed, he spent five years inside the institution before leaving in 2011 to join the Hoover Institution and teach at Stanford's Graduate School of Business. He arrives at the chairmanship with deep institutional relationships, firsthand experience steering the Fed through the 2008 financial crisis, and fifteen years of studied critique about what the Fed got wrong afterward.

What Will Change?

Warsh has described his agenda as "regime change" at the Fed, not a tweak to the existing framework, but a fundamental reassessment of how the institution defines its mission, measures inflation, and communicates with markets. Several specific priorities emerged from his April 21 Senate Banking Committee confirmation hearing. We’ve highlighted the main ones below.

1. A Refined Inflation View

Warsh is a critic of the Fed's 2020 shift to flexible average inflation targeting, the framework that allows inflation to temporarily exceed 2 percent, and favors reverting to a strict 2 percent target. He has also called for a broader reassessment of how inflation is measured, including the use of alternative methodologies. Under Powell, the Fed's preferred gauge has been core PCE (personal consumption expenditures). Warsh dismissed that measure as "a rough swag as to what was going on" with prices.4

For investors, a stricter inflation standard is ultimately a credibility play, one designed to anchor long-term expectations and reduce the kind of policy whipsaw that has rattled bond markets over the past several years.

2. The Balance Sheet: Prefer the Rate Tool

Warsh views the Fed's use of its balance sheet as having played an "unhelpful role" in achieving the dual mandate and would prefer to reduce its balance sheet assets that currently exceed $6 trillion. His preference is clear: when given the choice between tools, Warsh has said that “traditional interest rate cuts are fairer because they penetrate the cracks of the entire broader economy, whereas relying on the central bank's bloated balance sheet disproportionately benefits those who already hold financial assets.”

He signaled that any balance sheet reduction would be deliberate and gradual, acknowledging it took decades to build and will require time and FOMC agreement to unwind. Even a slow, methodical reduction would represent a meaningful departure from the Powell era and may put upward pressure on longer-term bond yields over time.5

3. The End of Forward Guidance

Perhaps the most disruptive change Warsh is proposing is the elimination of forward guidance, the practice of telegraphing where rates are headed months and years in advance. He has indicated he would seek to abandon the dot plot, which charts each FOMC member's projected rate path. He also declined at his hearing to commit to continuing post-meeting press conferences, a transparency norm Powell had maintained consistently.4

Markets have grown deeply dependent on forward guidance as a positioning tool. The dot plot and press conferences gave investors a reliable map of where rates were headed, sometimes quarters in advance. If Warsh follows through, FOMC meeting days become higher-stakes events. The longer-term implication, however, may be a healthier one, capital markets forced to anchor on economic data and corporate fundamentals rather than parsing a Fed chair's word choice. Removing the forward guidance crutch is part of a broader project: reducing political and economic bias from monetary policy and restoring the institutional independence that makes central bank credibility durable over time.6

What Stays the Same...And What Was Never Right to Begin With

Despite the rhetoric of regime change, several structural realities will shape how quickly Warsh can act.

The FOMC is not Warsh's to command. Powell will become the first outgoing Fed chair to remain on the board since Marriner Eccles in 1948, with his term as governor running through January 2028. He has been direct about his intentions: "There's only ever one chair of the Federal Reserve Board. When Kevin Warsh is confirmed and sworn in, he will be that chair. I'm not looking to be a high-profile dissident or anything like that." Powell's focus is protecting the institution from external legal threats, not obstructing from within.6

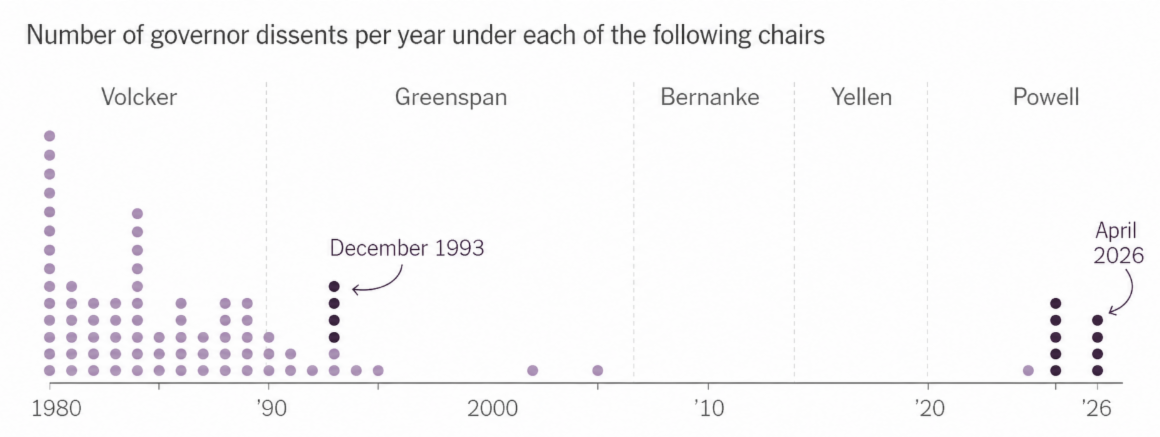

The rest of the committee may prove a more active constraint. At Powell's final meeting as chair, three regional bank presidents, Beth Hammack of Cleveland, Neel Kashkari of Minneapolis, and Lorie Logan of Dallas, dissented against language implying the next rate move would be a cut, signaling they were not prepared to follow a new chair's presumed preferences absent a clear shift in the data. Prior to the recent Fed meetings, the last time five or more FOMC members dissented in any form was the early 1990’s. For Warsh, dissent may be a feature, not a flaw. He has suggested that open debate inside the central bank can lead to better decisions and faster corrections when policy goes wrong, while also underscoring the Fed’s independence.

Source: Federal Reserve Board - Note: Includes dissenting votes on federal funds rate decisions.

The structural constraints on Warsh are, in important ways, features rather than bugs. His ability to achieve his goals will come down to his capacity to persuade holdover governors and FOMC members, not issue directives from the chair's office. More dissent, more deliberation, and more open disagreement within the committee is not dysfunction; it is an institution returning to something closer to its original character.7

The dual mandate is set by statute and is unchanged. The Fed's basic operating structure remains intact. And Warsh has stated that the conduct of monetary policy will remain strictly independent, and that the president never asked him to predetermine or commit to any interest rate decision.8

The Bottom Line

Markets are pricing mechanisms that price what they can see. A Warsh-led Fed intends, by design, to show them less. Fewer signals, less guidance, and a communication framework still being built mean capital markets will need time to find their footing under new leadership. Sinatra never needed the audience to warm up to him; he commanded the room from the first note. Warsh faces a different challenge: sixteen other voting members who haven't yet agreed to follow his lead. He may ultimately do things his way. But at the Federal Reserve, the Chairman of the Board still needs the band.

Principle Wealth