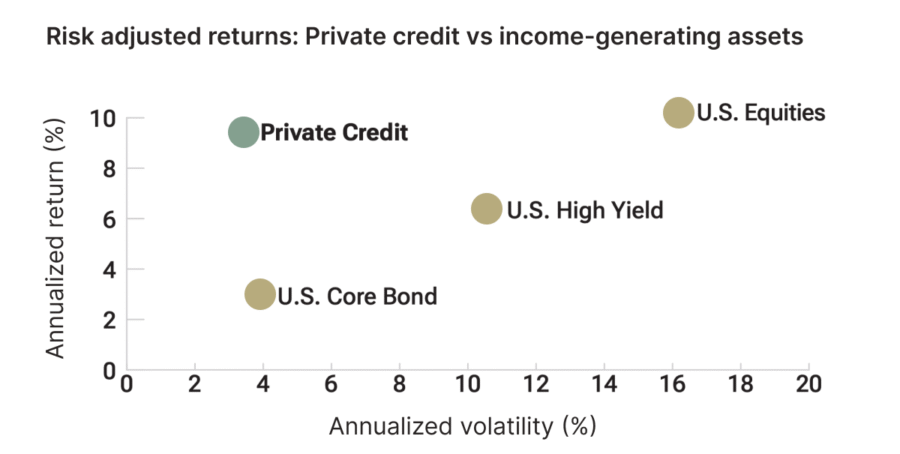

Private Credit: Smooth Until It Isn’t

Source: T. Rowe Price's and OHA's "introduction to private credit" white paper with OHA analysis as of June 30, 2023. Volatility is represented by standard deviation. Standard deviation measures the volatility of returns. Higher standard deviation represents higher volatility.

Private credit looks calm on the surface. That’s largely because it doesn’t trade. It’s often positioned as a private, bond-like investment, offering higher income with less day-to-day volatility.

The tradeoff? Limited transparency, limited liquidity, and often layered fees. These risks tend to stay hidden in stable environments. They show up quickly when conditions tighten.

That’s why we’ve stayed on the sidelines.

What is Private Credit?

Private credit is direct lending outside the public markets, where companies borrow directly from private funds instead of issuing bonds or borrowing from commercial banks. Often times, these loans are pooled and securitized in order to accommodate investments by institutions and individuals. Investors earn returns primarily through interest payments, assuming borrowers continue to perform with principal paid back at the end of the loan.

Why it Exists and Who Owns It

What we now call private credit used to go by different names: mezzanine debt, middle-market lending, private placements.

After 2008, increased regulation pushed banks away from lending to smaller and mid-sized businesses. Capital still needed to flow, so private lenders stepped in.

Over time, this evolved from a niche solution into a full-fledged industry. And like most financial innovations, it didn’t stop there.

Loans began to be pooled, packaged, and distributed, moving from institutional portfolios into retail-accessible products.

The typical investors in the Private Credit space are pensions, endowments, insurance companies, and large family offices.

These investors can lock capital up for years and have teams to evaluate managers, deal terms, and downside risk.

Today, individuals often access private credit through wrappers like Business Development Companies (BDCs) and interval funds. And the wrapper matters, because it determines what you can (or can’t) do with your money.

The Overlooked Risks (The Part Marketing Skips)

Source: Fitch Ratings

1) Liquidity Risk: The “You Can’t Sell When You Want” Problem

Private credit loans don’t trade like stocks or public bonds. If a fund offers withdrawals but owns hard-to-sell loans, you get a mismatch:

- Investors want ATM access

- The fund owns assets that take time to sell

- Sell loans (possibly at a discount)

- Borrow to meet withdrawals (adds leverage/risk)

- Limit withdrawals (“gate”)

Liquidity is not a feature of the asset class. It’s a feature of the wrapper, and those two don’t always align.

2) Fee Risk: The Silent Return Killer

Private credit often carries multiple layers of cost: management fees, incentive fees, fund expenses, and sometimes distribution-related costs. Even if the loans perform, fees can meaningfully reduce what investors earn net. In many cases, investors are paying public-equity-like fees for private-debt-like returns.

3) Credit Risk: What Happens in a Downturn

At the end of the day, it’s lending. Defaults tend to rise in recessions or during less liquid times in the market, especially among smaller, more leveraged borrowers, often private equity-owned. Outcomes depend on borrower leverage, the strength of loan protections, and the manager’s ability to navigate workouts and recoveries. Many borrowers are backed by private equity sponsors, which can add leverage and complexity in stressed environments.

4) Transparency Risk: The “Stable Price” Illusion (Marking Lag)

Private credit doesn’t have a live market price every second. Values are updated periodically using models and estimates, which can make returns look smoother especially during fast selloffs. Key point: A smoother return profile on paper can simply reflect delayed pricing, not reduced risk.

5) Correlation Risk: It’s Not as Diversified as It Looks

Private credit is often marketed as a diversifier. In reality, it is still economically sensitive lending. In downturns, defaults rise, recoveries fall, and correlations to other risk assets tend to increase, right when diversification is needed most.

6) Structural Risk: Wrapper vs. Asset Mismatch

Many investors access private credit through interval funds or BDCs that offer periodic liquidity.

The challenge: the underlying loans don’t match that liquidity profile. This creates structural tension between investor expectations and asset reality, especially during periods of stress.

7) Refinancing Risk: The “Extend and Pretend” Cycle

A significant portion of private credit relies on refinancing rather than full repayment. When capital is abundant, this works seamlessly. When capital tightens, refinancing becomes more difficult, and credit issues can surface quickly. In some cases, problems are delayed, not resolved.

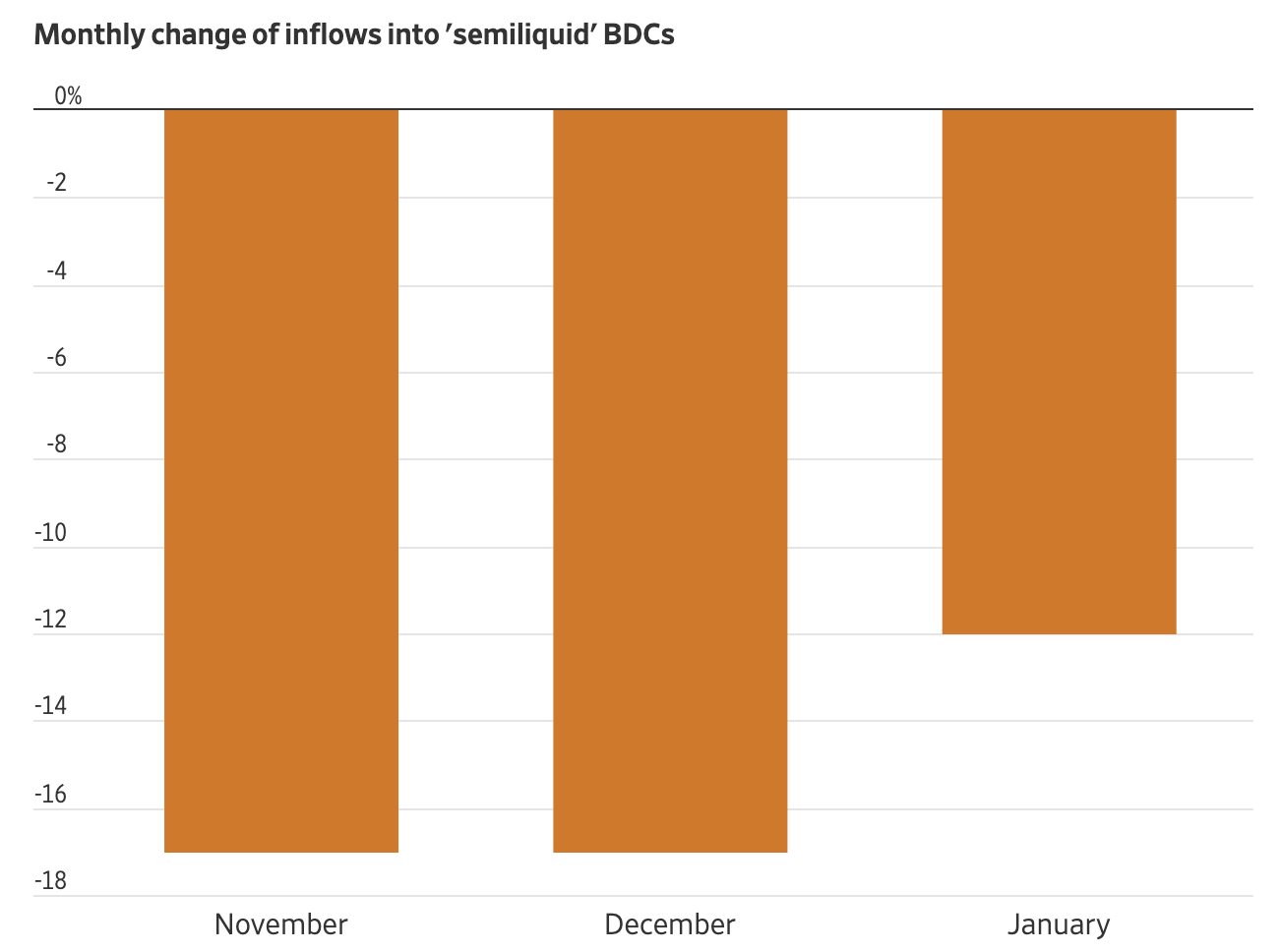

Blue Owl: A Real-Time Reminder of the Tradeoffs

Private credit hit the headlines after Blue Owl restricted withdrawals in a retail-focused vehicle as redemption requests rose. Investors wanted liquidity, but the structure couldn’t fully provide it. The answer, effectively: “not all at once.”

Separately, Blue Owl-affiliated BDCs announced the sale of roughly $1.4B of loans to institutional buyers, framed as an orderly way to raise liquidity.

You don’t need a view on Blue Owl specifically to get the message, it’s about the structure. Private credit works well when liquidity isn’t needed. The real test is what happens when it is.

And when liquidity tightens, everyone with exposure feels it, big or small, high-quality or not.

The “illiquidity premium” is often cited as a benefit. In practice, that premium may reflect a combination of:

- Higher credit risk

- Fee drag

- Slower price discovery

- In other words, investors may be compensated, but not always in the way they expect.

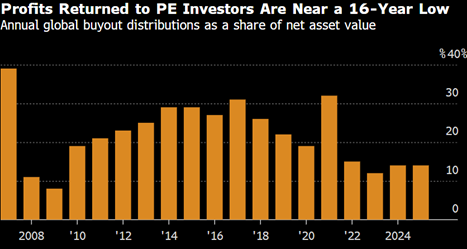

Why We Don't Own It

Source: MSCI. Note: 2025 represents the 12-month period from Q4 2024- Q3 2025.

We avoid private credit today for two simple reasons:

- Liquidity isn’t guaranteed when it’s actually needed

- Transparency is limited, both in pricing and downside risk

For most investors, the combination of illiquidity, opaque pricing, layered fees, and credit-cycle risk is not a tradeoff we believe is worth making.

We prefer liquid and transparent investments that are not only understandable in calm markets, but resilient during periods of stress.

Principle Wealth