The Supersonic Boom:

Operation Boomer and the Great Wealth Transfer

Source: AI Generated Image

The largest movement of private wealth in recorded history is already underway, and Boomers are in the driver's seat. Between now and 2048, Cerulli projects an estimated $124 trillion will change hands, and the decisions made by the generation that built that wealth will reshape the American economy, the structure of capital markets, and fiscal and monetary policy for generations to come.

The Supersonic Boom

The term "Great Wealth Transfer" undersells what's actually happening. A more accurate framing is a supersonic boom: accumulated capital compressing and moving through the economy at a speed and scale with no historical precedent. The closest comparison is the post-WWII economic expansion, but even that was a story of wealth being created. This is a story of wealth already created being redistributed, all at once, within a single generational window.

To put it in perspective: U.S. GDP in 2025 was roughly $31.4 trillion. The wealth set to transfer is nearly four times that figure, flowing through real estate, investment portfolios, private businesses, pension assets, collectibles, and cash, touching every corner of the economy as it moves.

The boom is already underway. The question isn't whether it happens. It's whether the people in its path, on both sides of the transfer, are positioned to handle it.

You Built It. Here's How.

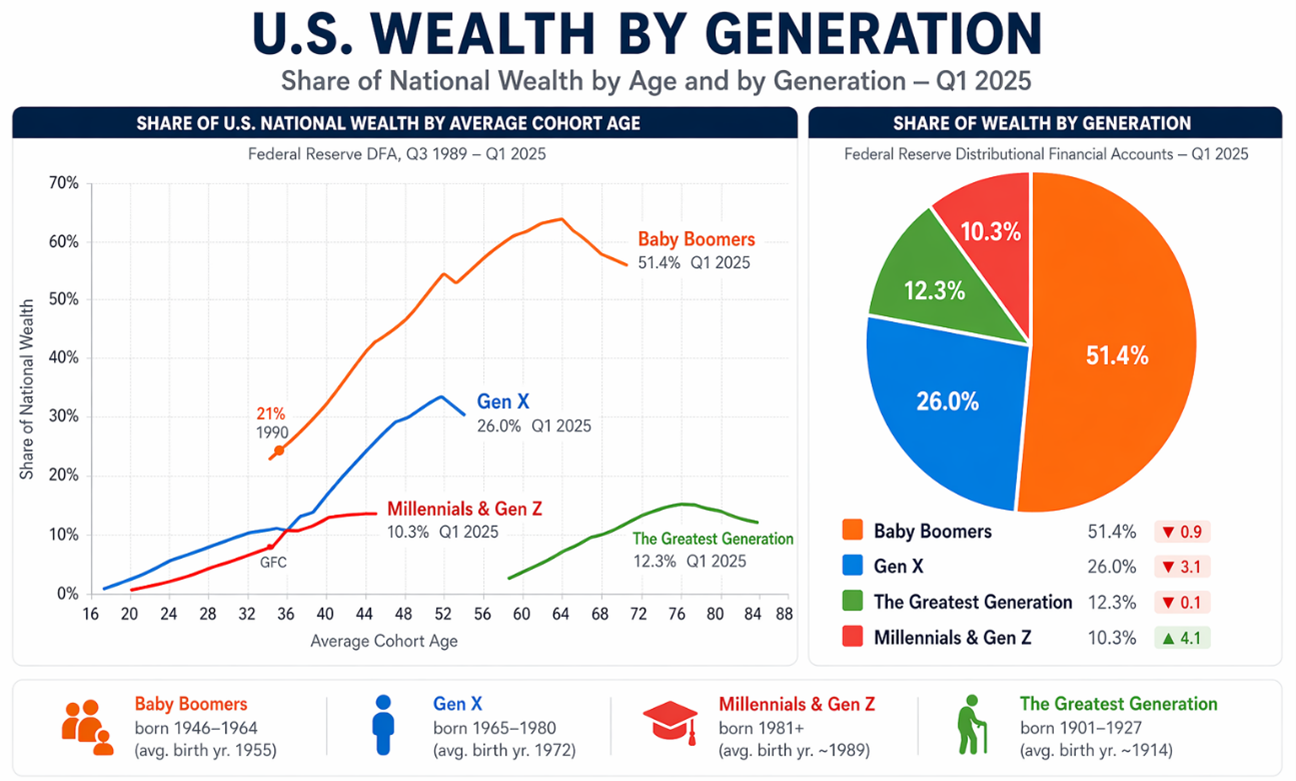

Source: Federal Reserve Distributional Financial Accounts (DFA)

▲▼ Change vs. prior chard period | Fed DFA: born before 1946 = Silent & Earlier; 1946-1964 = Boomer; 1965-1980 = Gen X; 1981+ = Millennial

Boomers currently hold 51.4% of total U.S. household wealth. But they didn't just accumulate wealth. They accumulated it within the most favorable structural economic conditions any generation has ever experienced, conditions that were, in large part, built around them.

Start with the macroeconomic backdrop. From the early 1980s onward, the Federal Reserve presided over a sustained 30-year decline in interest rates, from a peak federal funds rate above 20% in 1981 to near zero by 2009. Falling rates were a tailwind for every asset class Boomers owned: bond prices rose, equity valuations expanded, and real estate climbed. Each of those assets was already in Boomer hands.

Fiscal policy compounded the effect. The Reagan tax cuts of the early 1980s, the capital gains rate reductions of 1997, the Bush tax cuts of 2001 and 2003, each iteration reduced the tax drag on the investment income and capital appreciation Boomers were accumulating. Whether by design or coincidence, the system supported the creation and expansion of wealth.

Then came the pandemic. From 2020-2023, equity markets grew 27% and real estate surged 39%. A generation already holding the majority of national wealth saw its balance sheets expand dramatically, just as this transfer window was opening.

The youngest Boomers are now in their early 60s. The oldest are approaching 80. The handoff is ramping up.

Earn vs. Inherit: The Fundamental Shift

Source: AI Generated Image

For most of American economic history, wealth was primarily earned. People worked, saved a portion of what they made, invested it, and built assets over a lifetime. Wages were the dominant input to household wealth. The 21-to-31-year-old employment cohort mattered enormously because young workers entering the labor force fueled consumer spending, housing demand, and economic growth. Their wages became consumption. Their consumption became corporate revenue. Their employment rate was a reliable leading indicator of where the economy was headed.

That model is eroding in real time.

When $124 trillion transfers to the next generation over the coming decades, inherited wealth becomes a parallel engine of economic activity, one that operates independently of the labor market.

A Gen X household that inherits millions in assets doesn’t need to earn that capital. It’s wealth without wages. It arrives fully formed, with built-in liquidity, income potential, and financial flexibility. And when that capital is deployed into markets, real estate, private investments, or consumption, it generates demand that has little to do with whether that household is working.

This is structurally new. The American economy has never experienced this scale of simultaneous wealth transfer. And it changes how we answer the questions economists and investors have asked for decades, while also challenging the reliability of the data those answers have long depended on.

What Actually Happens When Wealth Arrives

Here's what the research shows, and it's more complicated than most people assume.

Wealth that is earned arrives with something attached to it: habits, discipline, and a framework built around accumulation. The person who built it knows what it took. They have a felt relationship with the capital that shapes how they manage it.

Wealth that is inherited arrives without any of that. The same dollar, in the hands of someone who didn't earn it, tends to behave differently. Studies consistently show that large windfalls, particularly inherited ones, are associated with reduced labor force participation, lower savings rates, and a higher likelihood of lifestyle inflation rather than compounding. Approximately one-third of inherited assets are consumed rather than invested within two years of receipt. That isn't a moral judgment. It's a behavioral pattern with economic consequences.

For Boomers thinking about what to transfer and how, this matters. It also raises a question that doesn't get asked enough: does the arrival of inherited wealth diminish the drive that built it? When a generation no longer needs to earn more or work harder to achieve the financial standing their parents worked a lifetime to reach, what happens to motivation, to financial discipline, to the habits that produce long-term wealth in the first place? The honest answer is that inherited capital and earned capital don't produce identical outcomes. How wealth is transferred matters as much as how much is transferred. Structures that build financial competency in heirs, rather than simply delivering assets to them, produce better long-term results on both counts.

The Conversations That Need to Happen Now

Talk to your heirs before the transfer, not after. Heirs who understand where the wealth came from and what values shaped it are more likely to steward it well. The conversation is the first act of the transfer.

Understand what your spouse would face alone. The first transfer is almost never to your children. Does your spouse understand the full financial picture? That question deserves an honest answer before it becomes a crisis.

Compare your documents against current law. Anything drafted before 2020 is likely out of date in at least one material way.

Don't mistake inaction for neutrality. The transfer happens one way or another, with a plan or without one. The difference almost always comes down to whether the work got done.

Principle Wealth